Open banking

How Pay by Bank can reverse the impact of card declines

Failed card payments are problematic on two counts. For shoppers, they’re concerning and inconvenient. For merchants, they’re a revenue blocker. And while they’re simply a fact of life in the e-commerce world, their impact can be reversed – on both sides – by the right payment recovery tool.

Why card payments fail

It’s first worth unpacking why card payments fail, with reasons falling into one of two types:

- Hard declines, which are initiated by the card’s issuer. When someone tries to use a lost or stolen card, and it’s been reported, it’s a hard decline. Payments cannot be attempted again.

- Soft declines, which occur when there’s a processing issue, when the payer fails to authenticate their identity, when an acquirer suspects fraud, or when the card has insufficient funds. Payments can be attempted again.

The impact of failed card payments

It’s a scenario that is far too common; according to research, 40% of consumers across the globe had a payment wrongly declined in the three months prior. When we look at some market specifics, 56% of shoppers in the US had their payments declined when shopping online in 2023 alone, followed by 48% in Singapore and 45% in the UK.

These declines can have detrimental effects on a merchant:

Revenue loss

Dato Insights calculated the average false decline rate at 1.5% of e-commerce sales, which - when it comes to revenue - is predicted to reach a loss of almost USD 265 billion by 2027. Despite these worrying numbers, 82% of merchants claim it’s difficult to determine the cause of the failed payments, with 56% admitting these payments are expensive to track and resolve.

Lost customers

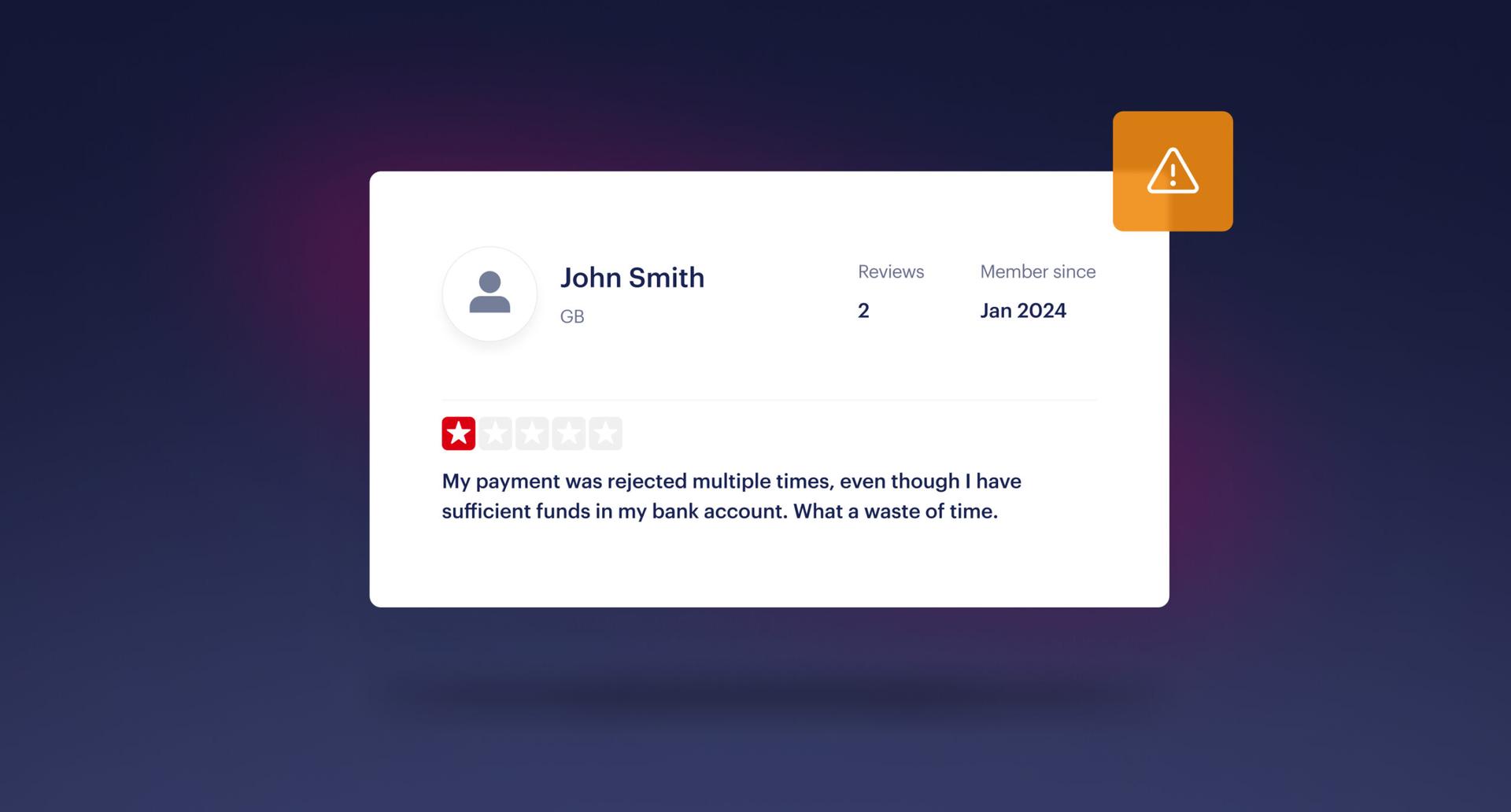

If a customer who knowingly has sufficient funds in their bank account has their payment fail at checkout, chances are they will be insulted and frustrated by the situation. In fact, four in 10 customers say they won’t shop with a merchant again if their payment is falsely declined.

Negative brand reputation

Consumers are willing to spend around 46% more with a retailer that they trust, proving how important reputation is to revenue. Unhappy shoppers can deter new customers with negative reviews online (over a quarter of survey respondents would take their complaints to social media) and by word of mouth, creating a vicious circle which leads back to lost revenue.

Putting these into context, let’s say a customer tries to pay for a new pair of trainers using their credit card, but it fails due to a technical issue. They’re invited to try again but the problem reoccurs. They really want the trainers, and the merchant naturally wants the customer to convert, so what happens?

Without an effective payment recovery method, the sale is lost. The customer will run out of patience and look elsewhere. The impact, then, isn’t just short term. The merchant is likely to lose the customer to one of their competitors – for good. Customer lifetime value shrinks to zero, as does the likelihood of any word-of-mouth recommendations.

Open banking as a payment recovery tool

The reasons for failure expose the flaws inherent to card infrastructure, especially when compared to the benefits of real-time account-to-account payments:

No expiration or lost details

As opposed to a card, bank accounts cannot expire. Similarly, given a physical card isn't needed to ‘Pay by Bank’, the shopper doesn't have to worry about losing their card and being unable to input the details.

Lower risk of fraud

In terms of them being ‘stolen’, it’s true that account takeovers do happen. But because Strong Customer Authentication (SCA) is embedded into the open banking payment process, it’s extremely difficult for fraudsters to initiate e-commerce payments. [Learn more about how to use ‘Pay by Bank’ to combat fraud here].

Customers only spend what they have

Open banking utilises two types of account programme interfaces (APIs), one of which is an account information services (AIS) API. This enables regulated third parties to retrieve the balance of a customer's bank account, ensuring a merchant knows if there is sufficient funds. This eliminates the chance of a payment bouncing due to insufficient funds, or a customer needing to dip into credit.

Lower chance of processing issues

Further, with ‘Pay by Bank’ processing problems are much rarer owing to the lack of intermediaries. Since the payment comes straight out of the shopper’s bank account and lands in the merchant’s in real time, there is no need for the likes of card schemes or acquiring banks.

Seamless cross-border payments

When a shopper is in one country, and the merchant in another, card payments have even more intermediaries. The more points of call for the payment to pass through, the more risk of one point failing and taking the transaction down with it. Using a regulated open banking provider like Volt, we smart-route the payment for the best possible chance of success, meaning no reliance on a single bank connection.

All of these features make open banking payments a highly effective recovery tool for failed card payments. [Minor diversion: we’re using ‘real-time payments’, ‘account-to-account payments’ and ‘open banking payments’ interchangeably here. See this post for a detailed breakdown of each term.]

In 2023 the value of global open banking payments hit $57bn. By 2027, only three years from now, their value will increase to $330bn. A viable alternative to cards hasn’t just been found; it’s being adopted at a rate that’s truly unprecedented, on a global scale.

Inviting customers to ‘Pay by Bank’

There are two easy ways for a merchant to prevent card declines, and recover those that fail:

1. Offer ‘Pay by Bank’ at checkout

If a merchant has enabled open banking, it can simply serve a pop up inviting the customer to ‘Pay by Bank’ instead. It’s been found that merchants offering open banking at checkout can see up to a 20% uplift in conversion rates.

2. Send reminders to invite customers back

If the customer has already navigated away from the checkout, an email or text can be sent: ‘Your card payment failed, but don’t worry – you can Pay by Bank to secure your order.’ Land this message at the right time, in a way that plays to the customer’s preferences, and they’ll complete their purchase via a payment method that’s naturally faster, easier and more secure.

Furthermore, our data tells us that 80% of customers who try an open banking payment make a repeat purchase within one month. In other words, it directly contributes to increasing customer lifetime value – while also overcoming failed card payments and enabling merchants to avoid high card interchange fees. Is it any wonder that adoption rates are predicted to be so high?

Interested in using open banking as a payment recovery tool? We’d love to hear from you.

More like this

Open banking

Industry deep dive: Exploring player behaviour trends in eGaming

We uncover the latest player habits shaping the eGaming landscape, and how open banking delivers on the demand for superior in-game payment processes.

Open banking

How much are card fees: A complete guide to processing costs

From interchange fees to scheme costs, we explore the full set of expenses that come with accepting card payments - and how they can be avoided through open banking.

Market insights

From screen scraping to PSD3: The growth of open banking in DACH

We look at open banking in DACH, starting with the German Federal Post Office’s experience to the upcoming PSD3 and Payment Services Regulation.